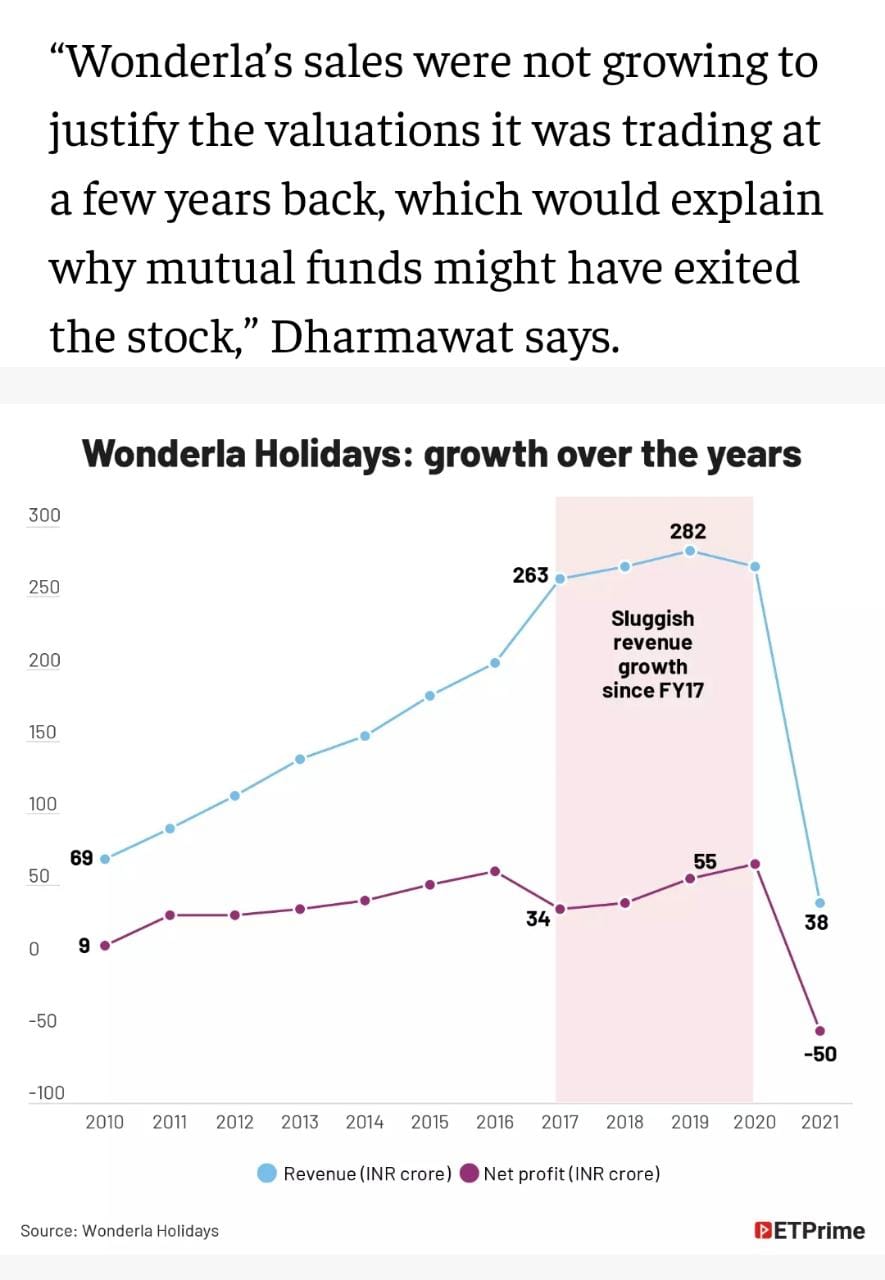

Niteen S Dharmawat, co-founder of Aurum Capital, quoted in this article in Economic Times on Jul 8, 2021

Niteen S Dharmawat, co-founder of Aurum Capital, quoted in this article in Economic Times on Jul 8, 2021

Attached is the link to the interview.

Our co-founder, Niteen S Dharmawat, is featured in money9 magazine.

Regards,

Aurum Capital

It was fun to present this at a TIA online event on Aug 1, 2020.

This is related to contrarian investing, especially in cyclicals. How one can try to evolve a strategy of when to invest in these stocks and importantly, when to exit. With case studies and also a current view on different sectors

-Jiten Parmar

Here is the video link of the presentation by Niteen S Dharmawat made at CFA Institute in Mar 2020. Time: 126mins

Watch @niteen_india, co-founder, @CapitalAurum, present "How to Avoid Common Mistakes and Uncommon Losses" at an event organised by CFA Society India, Pune chapter.

Link: https://t.co/k490YphJgJ pic.twitter.com/b6LoW0TnuF

— CFA Society India (@CFASocietyIndia) April 6, 2020

The link to the video recording of the event is in the tweet.

@niteen_india will be in conversation with Dr @anillamba03 on his latest book "Financial Affairs of the Common Man" on 29 Feb (tmorrow), Saturday, at BDB Club, MCCIA Trade Tower, SB Road, Pune.Time 11:00am onwards.

This event will be live on @teamkpoint: https://t.co/mpBmrD8OCw pic.twitter.com/zCOZoQgB7v

— Aurum Capital (@CapitalAurum) February 28, 2020

Enter your email address for unsubscription.

Subscription to our blog and newsletter